I read that half of Americans couldn’t cover an unexpected $1,000 expense. This sounds crazy to me. I understand that poverty exists, but the idea that an adult with a job doesn’t even have that amount saved up seems really strange.

What’s your relationship or philosophy with money? What do you credit for your financial success, or alternatively, what do you blame for your failures?

For the extra brave ones: how much savings do you have, and what are you planning to do with them?

You must log in or register to comment.

I have enough in my emergency fund that if I lost my job I’d be ok for about a year.

I’m nearly to my goal, after that I’m going to change my focus to expanding my portfolio.

Still no way I can buy a house though. Need to make about 3x more money for that to happen.

I credit it to having a property owner that’s kept rent cheap and having low overhead, and being frugal borderline cheap.

I’m doing well at the moment. The problem is that no matter how well I do, eventually something destroys my savings and eventually there’s a layoff at my company.

Even if I’m doing well at the moment, I’m still a couple paychecks from not doing well, and am no where near on track to eventually be able to retire

I have five digits of savings for the first time since my kids were born, but I also have college expenses for them, and at least that much in deferred house maintenance

I credit Apple, of all things. I always chose credit cards to minimize interest and fees, so this is the first time I’ve had one with significant cash back. Now I pay essentially everything with Apple credit card, pay off at the end of the month, get a surprising amount of cash back, directly into the high yield savings account. While of course my job is the reason I’m doing well, I credit this for turning things around to actually let me put money aside, to boost my savings

Im doing well. Started off in my mid twenties reading books on finance and investing. Lived in a drug house where I rented out a room and had a dead end job. Got an education, decent job, and invested aggressively for the next 20 years. Im planning on retiring in my mid 50’s if everything goes to plan. 🤞

I am one broken leg away from being homeless and losing everything, and it’s been like that my entire working life. I’ve never been able to make enough to actually save. Currently I have -100 in the bank and some debt I’m trying to pay off on top of that. My rent is literally half my income.

I dislike money. I worked hard to have enough that it’s not on my mind. I don’t need to think about the cost of eating out or buying food, or pursuing hobbies. But I also don’t really spend much. I don’t make big purchases very often and when I do I still over-analyze them.

If I had a lot more money I could retire, but I still have half my life to live. I hope to retire in 16 years. I have a job that pays well, with good job security, and minimal stress. I get 38 hours of leave time per month and I live in California.

I have cash savings earning enough per month in interest to pay my cell phone and home internet bills entirely. But I don’t really have any other discretionary monthly subscriptions. My savings will probably be used on a new kitchen and bathroom eventually.

I was born at an unfortunate time. By the time I could afford a house the housing market was already very bad. I’m just glad I’m able to buy a house but it is very expensive (we bought at the end of 2021)

I live in Canada so we can’t lock in our mortgage for more than 5 years. I just went with the variable rate because in the long term it’s generally better. However the interest rates skyrocketed. I was able to pay my mortgage still but I was pretty much house poor.

Now the rates are finally dropping so I feel a lot less pressure. With our current budget we should be able to afford one kid comfortably. I’m not sure about a second.

I’m very fortunate and grateful though. Most people my generation cannot even afford a house. It’s just insane that despite my great job it’s still so hard for us I can’t imagine what others are going through.

We aren’t broke. I have some retirement saved but I had to stop putting money in due to our mortgage. I also have an emergency funds account with enough money to sustain us ~6 months if I were to lose my job.

Having a high paying job is unsurprisingly the main reason for my financial success. Otherwise I’d say joining some personal finance clubs helped a bunch. I have my savings diversified and invested so I’m at least not losing money to inflation. But my investments will never make me rich either.

One critique I have for myself is maybe we overspent on the house but at the same time I love our neighborhood and I love our house and we have no plans on ever moving so I’m not too upset by it.

I’m doing well but i wish i could afford my hobbies.

Financially, we are well enough to have my family’s needs met comfortably but frugally. Can’t really ask for more, though additional breathing room would be nice. We can afford emergencies and recover after some time.

My parents and grandparents taught frugality; luck made ends meet like a good job and buying a house at the right time.

We have a bit of savings I have in mutual funds because I’m currently too mentally tired and risk-averse to pick something with higher return potential.

I credit my success to some hard work but mostly luck. At the end of the day my first job was from a recommendation. I believe interviewed well, sure, but I don’t think they would’ve taken my resume otherwise. I’m extremely fortunate to be where I am financially.

Shit still happens though. I lost my job about a year ago and was unemployed for like 6ish months. I had enough money in savings that it didn’t really matter but it still sucked. One thing that has been difficult for me is watching what I say. As an example, some stupid shit happened and I feel like a company owes us ~$800 and another one ~$200. (Not going into details because they’re irrelevant and I want to move on from the stress.) These things royally pissed me off. I still get upset when little things happen and I lose money. I hate it. It sucks. As much as I want to get comfort from my friends by venting about it, sometimes it’s better to shut up. Because some of them mostly just hear how I’m able to withstand losses like that and that in turn makes them feel upset that they aren’t. It’s a tricky thing.

As for my philosophy, for the most part my wife and I have been able to spend within our means without much aggressive or intentional budgeting. It’s only been since the job loss and her being unemployed to pursue writing a novel that things have gotten tight. (And by right I just mean our savings aren’t noticably increasing.)

Failures? Well, let’s ignore stuff like crypto and stock picks because that’s just gambling. I wish I had started maxing out my 401k in my 20s. I started on my early 30s. Also, we used to have a truly stupid amount of money in a checking account. We should’ve put it into stocks (as in total market ETFs) earlier.

OH. THIS IS IMPORTANT. I WISH SOMEONE WOULD’VE TOLD ME HIGH YIELD CHECKING ACCOUNTS EXIST. Like, holy hell. I should’ve done that ages ago. I don’t even wanna think about how much money I’ve lost on, especially because we kept a stupidly high amount of cash in our checking account… I still haven’t moved it because it’s hard and I’m lazy but wow wow wow. This is stupidly important. The reason savings accounts are annoying so because it’s a little harder to get to your cash. But a checking account with interest? Hot damn.

Lastly, I’ve never had a credit card. It’s been fine but it would’ve been nice to get the tiny marginal benefits of cash back and stuff.

Why does everyone think it’s this huge hassle to open a new checking or savings account? Takes like 30min.

It is a huge hassle to move every single auto pay, deposit, etc. to a new account.

Ah yeah I guess it’s easier when everything is on a credit card and you just use your checking to pay off your credit card.

I have $15.

Not just that I can spend. Not “until sometime in the future.” Just $15.

feel ya. i had $8 left before my last payday and I’m guessing it’ll be like that before my next payday too.

Im doing pretty well. Living in Germany, educated parents. Did okay in school, never studied much though. Went to university, got my Masters in Mathematics (needed to study a lot for that, but its my passion anyway). Started working at an IT company in the same city.

3 years later, I have around 50k in savings now. We live in a small apartment, are in the middle of buying a house.

Capitalism is really fckd up, especially in the US. I try not to take advantage of it too much, up my monthly donations with every raise, vote left-ish, dont support big corporations.

I think the biggest factor for success is luck for being born under the right circumstances. Thats like 99%, the rest is having some self control.

I’ve got $0.85 in savings, because I put my rent and car payment money in my savings account each month until I need to pay those bills. I did at one point have $1000 saved up as a rainy day fun, but then it rained for a whole year (financially speaking). Now I don’t even have credit cards to fall back on, as those have been maxed out and gone to collections. I’m looking for a job in an industry I left because it was driving me to alcoholism (software), but that job market sucks a little more than the service industry, so I’m not optimistic.

Oh yeah and I’d be homeless if I didn’t have family who were willing and able to loan me rent money.

I currently work on software in automotive. Everything seems completely insane. We have tons of process and technical debt, executives that are super out of touch and all have their own pet projects, we have hundreds of executives so we have 100 number one priority pet projects, we have a very distributed hardware/software footprint due to the affirmationed process/technical debt, each vehicle has a different hardware footprint which means we constantly have to make our distributed software work when a piece of the software needs to be rebuilt in a new controller, etc etc.

There’s also the whole mess of trying to run agile at scale, managinga very distributed backlog, trying to balance priorities across teams that have to coordinate work, everyone leading with “how they want it” instead of “what they want”, total disregard for WIP limits, etc.

I know where I work is a shit show. I really wonder if it’s much better elsewhere. I also wonder if this place has always been a shit show and I just have more exposure to it now.

And yeah, alcohol. I’m trying to cut back but the mood here seems to violently oscillate between “this is OK” to “what the hell” and back again. We’re probably due for another swing soon.

Some days I do think about going back to waiting tables. It took me years of working elsewhere to stop having the waiting weeds dreams though…

I know where I work is a shit show. I really wonder if it’s much better elsewhere.

Have you seen the state of almost every piece of software nowadays?

Hence my wonderment, lol. I meant more organizationally, but if you’re putting out a crappy product things probably aren’t great working there.

I’m digging myself out of a $13k credit card debt hole. I burned through my savings when a job that I had ended on my unexpectedly, and because it was contract work I wouldn’t qualify for benefits. They kept me around as a sub, promising me a full time position if I just stuck around long enough and I was foolish enough to believe them.

I’m self employed now and making do with the best I can, but I’m planning on ending my dream as a musician/ teacher and moving home. I don’t know who would want my skills, but I know they are specialized and strong. I just gotta see what kind of work would value them.

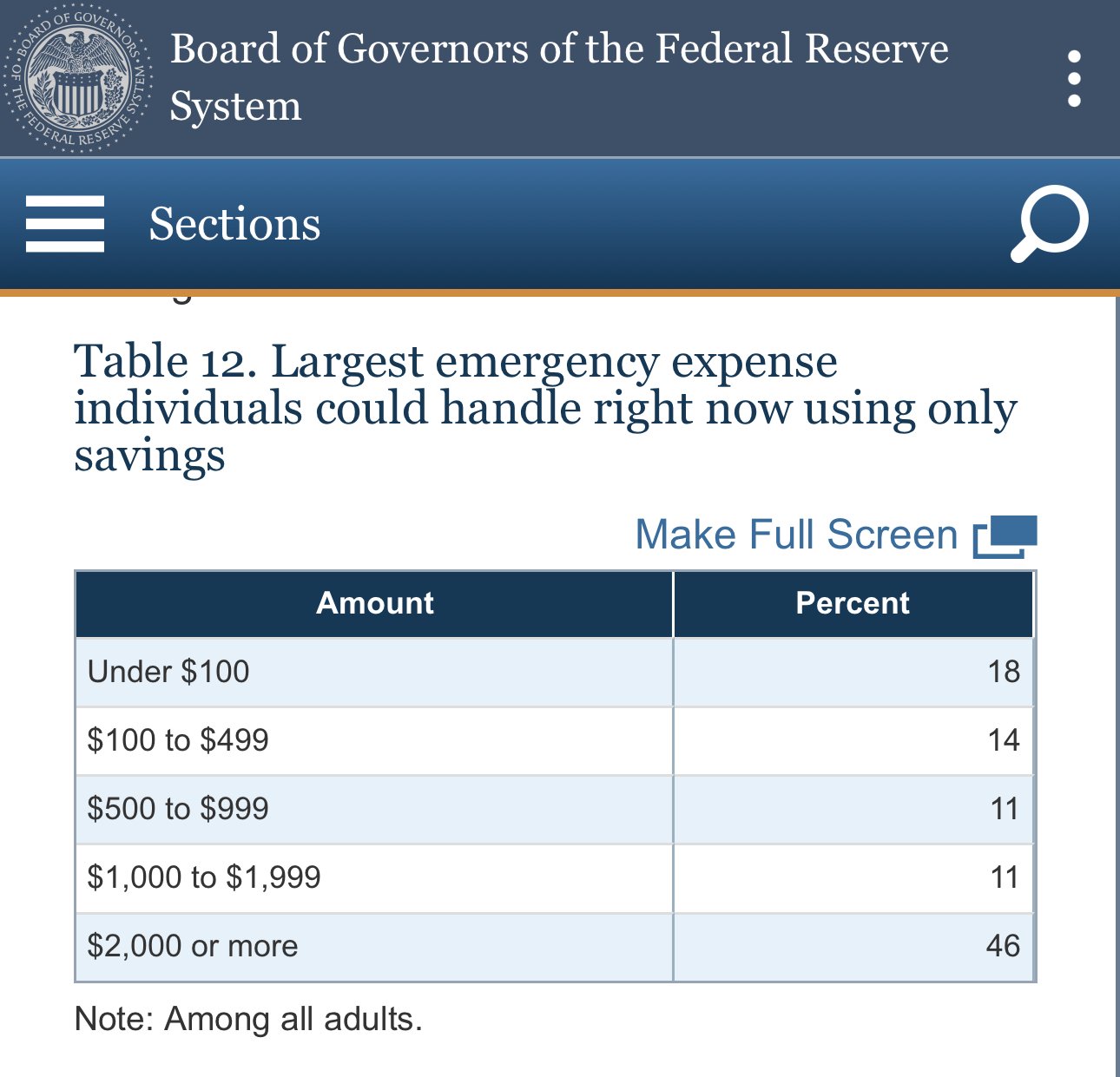

They release data for stuff like this. Currently 46% can cover a cost of $2K or more with just savings. 57% for $1K or more.

But it’s even worse than that - what kind of emergency is that cheap? Sure I could replace tires in my car within that amount, but could not repair a car accident. I could visit an ER within the amount but could not pay for medical care for sickness or injury. I could call a plumber within that amount, but not not repair or replace things after a leak. I could travel to see my elderly Mom if she were sick, but could not afford a place to stay there within that amount

What’s your relationship or philosophy with money?

A life-changing shift to my approach has been to worry about absolute amounts rather than percentages. Saving $10 on a $20 item feels great but ultimately is the same thing as saving $10 on a $500 item (which feels like nothing).

I grew up lower middle class: never had to worry about not having a roof over my head, but there were times we were somewhat food insecure, and spending money on leisure/entertainment or anything unnecessary for survival was a foreign concept until I got to high school and some my parents’ career moves paid off and put us in upper middle class. It took them a good 10+ years before they could relax a little bit and feel secure with their money, though, and that was as much driven by the fact that their kids were adults who had moved out.

So life has been about deciding which of my parents’ frugal attitudes and approaches to money to keep and which to discard.

Things I decided not to adopt:

- I slowly learned to stop caring as much about wasted food. Food is just cheaper now compared to when I was growing up (even if the last 5 years has shown an uptick), and as a society we have more issues with obesity than hunger, so cleaning off a plate seems like it doesn’t actually do that much good.

- My time is worth something to me. I will gladly pay the few dollars here and there for convenience.

- I’m glad I ignored my parents advice to buy a home as soon as I could and build equity or whatever. I rented and it worked out great for me, giving me the flexibility to make changes at different stages of my life.

Things I kept:

- Life is uncertain. Always be prepared with whatever you can accumulate for financial resilience: cash, other property, lines of credit, marketable job skills, literal insurance policies, etc. Don’t underestimate the importance of personal relationships, whether it’s “credit” from friends and family who can help you out of a bind, colleagues who can refer work to you, bosses who will fight for your career, etc.

- Develop your career. Education and credentials are important early on, and up-to-date skills and a good understanding of the landscape in your field (both in the type of job and the type of industry you work in), plus solid relationships with people, can help you know when switching jobs is right for you.

Things I had to learn on my own:

- Life is unfair. Many types of unfairness are systematic. So why not position yourself to where the unfairness works in your favor, if available?

- Higher income makes it easier to survive mistakes on the spending side. To flip around Ben Franklin’s quote, a penny earned is a penny saved.

- Know yourself and your own laziness. Set up automatic functions wherever possible: automatic bill pay, automatic savings, automatic investments, etc. Steer away from any strategy that requires active management, and towards strategies that tend towards a set it and forget it philosophy.

I’ve also made a shitload of mistakes, some of them pretty costly, especially back in my 20’s:

- Paid probably thousands in credit card interest in my early 20’s chasing lifestyle bullshit.

- Paid thousands in unnecessary car loan interest in my mid 20’s by getting suckered by a dealer.

- Paid hundreds, maybe thousands, in late fees and interest from forgetting deadlines to pay shit I actually already had the money on hand for.

I’m rich now, most of it from luck (especially timing), much of it from personal relationships (good family, good marriage, good friends), some of it from actual effort (good grades from a good law school), and some of it from conscious decisions to steer towards my strengths and away from my weaknesses (lazy but smart, prototypical “gifted” slacker with undiagnosed ADHD).

It took a while to get here, though, and I was financially insecure well into my 30’s. Sorta figured shit out then, and then married someone who complements me pretty well on these things, and covers my blind spots.

For the extra brave ones: how much savings do you have, and what are you planning to do with them?

I have some savings, and it’s an emergency fund. It’s representing 1-2 months of typical spending, that could be stretched to 3-4 months if I needed to stop the frivolous spending. But I have credit beyond that, and less liquid assets I’d be able to tap into if I were facing a longer term issue.

But I’m not saving for any particular thing other than retirement. If things accumulate and grow, great. I’ll make a judgment call on when to retire based on how I feel and how much I have and what I want to do. I anticipate my wife and I will probably want to retire in our early 60’s, based on our anticipated career trajectories and the ages of our children.

Really interesting read. Thanks for the response.

Why do you only have a few months’ worth of savings despite considering yourself rich? Or are you just speaking about cash reserves?

Or are you just speaking about cash reserves?

Yes. Cash reserves are like unused RAM to me: I have it, so I might as well put it to work. If it turns out I need it somewhere else, I can always go rearrange things to make that possible.

Realistically, I think I’m rich because my wife and I both have strong ability to command high salaries, switch jobs, etc., even in a pretty severe downturn. The main things that might tank the value of that expected future cash flow are disability or death, and we at least insure against those.

We also only need one of our two incomes to support our lifestyle, so we have a certain resilience that just comes from having that buffer. At our current ages, we also already have substantial retirement savings, so we have some resilience there, too.

The but about higher income making it easier to have mistakes is a big one.

I have a friend online who wants to make money, but doesn’t seem to have the ability to do so without going back to school. Going back to school would incur student loan debt, so they do not wish to do so.

I have a crazy amount of student loan debt, maybe $150k. But people don’t understand that federal student loan debt is absolutely nothing like credit card debt. There are basically no downsides to it besides paying another monthly bill (that you can use an income based repayment plan for).

People don’t understand how incredibly useful excess income is even if it ends up with a lot of loan debt. I had a similar hesitancy back before I went back to school, but I don’t regret it at all. I think I ended up like tripling my income.

Even if you end up with a lot of loans, making say $80k/yr is astronomically easier to survive on than $40k/yr for example. You have to think that something like rent or food prices are going to be somewhat similar in your area no matter how much you make. Sure, you could choose to live in a lavish place I suppose, but if you live reasonably then it’s more than worth it.

As an example, the average rent price for a not shitty one bedroom apartment in my area is maybe around $1.6k, which would equate to $19.2k/yr. That’s almost 50% of the gross income of the person making $40k/yr while only around 25% of the person making $80k/yr. So even if the person making $80k/yr has a $1k/mo student loan bill (you can get it cheaper if you wish), the difference is dramatic.

The person making $40k/yr will have a little over $20k left over at the end of the year for remaining expenses and savings, but the person making $80k/yr will have more than double that at $48k left over. Obviously there are a lot of nuances in this but still.

So it’s absolutely worth it to incur federal student loan debt if it means you will make a lot more more money. Private loan debt is a bit different.

Yeah, I’m not going to pretend like I’m good with money. I’m not. I have a decade of experience of being a young adult on a tight budget to know that’s not one of my strengths. I wasn’t great at stretching each dollar to its most efficient use. And I still am not.

I won’t speak on whether student loans are worth it. I think, like everything, it depends. I think a bachelor’s degree is definitely worth the cost (both in tuition and time), but it might still be worth doing it cheaper if there’s a cheaper path available.